Some strange things are afoot right now in the product world. (And I suppose consequently at the Circle K.)

New pressure is squeezing consumer product companies from both sides.

Investors demand steady performance and cost reduction in the face of tariffs and inflation.

Consumers demand innovation and value.

Retailers expand their private labels while controlling shelf space with unprecedented power.

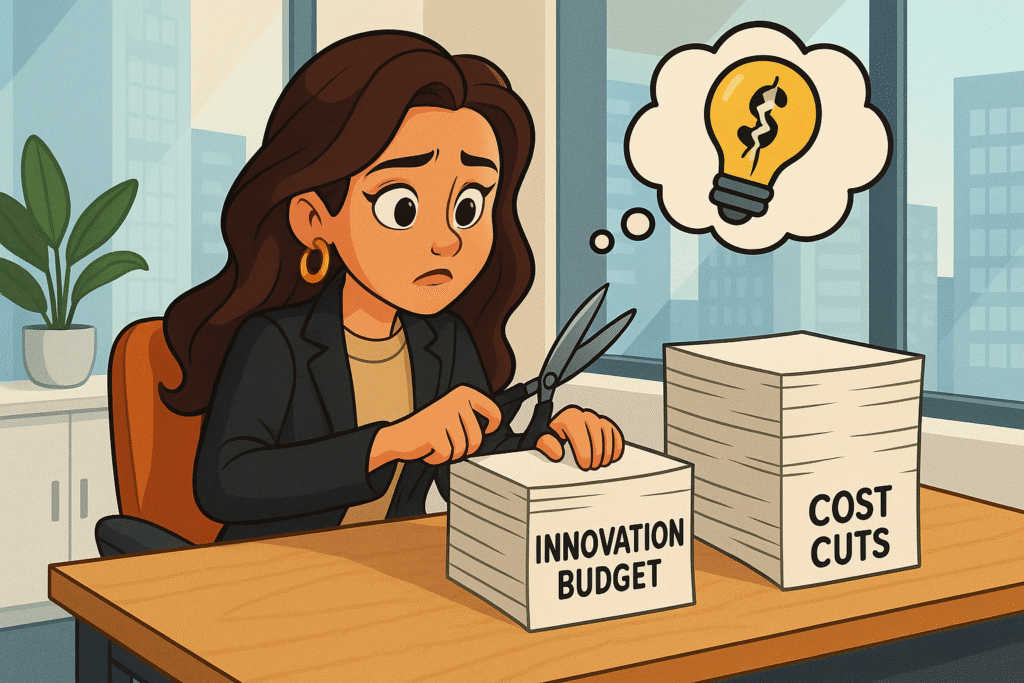

Something has to give — and in my experience, it’s usually the WRONG thing.

A brand new EY report surveying 190 global CPG CEOs reveals a dangerous pattern: 65% acknowledge their strategies are increasingly shaped by investor expectations rather than customer needs.

When volume drops and growth stalls, the knee-jerk response is cutting innovation budgets and pursuing cost-saving mergers.

This starts up a death spiral DISGUISED as prudent management.

Companies reduce R&D spending right when they need breakthrough products most.

They focus on incremental cost savings while nimble challengers capture market share through superior innovation speed.

They optimize for quarterly earnings while their long-term competitive position erodes.

The retail landscape’s structure makes this even more deadly.

A stunning 78% of retailers believe their shelves will eventually feature just one mass-market brand per category, with the rest dedicated to private label or niche offerings.

Think about what that means: in most categories, there’s room for exactly ONE major brand to survive the private label onslaught.

This is a preview of what happens in any industry when financial engineering replaces product innovation as the primary strategy.

In I Need That, I dive into how sustainable competitive advantage comes from solving customer problems better than anyone else, not from optimizing cost structures while offering identical solutions.

Product Payoff: While traditional beverage companies were busily stomping on innovation budgets, Liquid Death exploded from zero to $1.4 billion valuation by approaching the most boring category imaginable — water — with relentless product innovation. LD’s punk rock branding, limited edition releases, and category-defying marketing proved that even commoditized markets have room for breakthrough thinking.

Meanwhile, established beverage companies focused on cost optimization and incremental improvements, coughing up market share to an upstart that understood innovation drives growth more reliably than efficiency gains!

Action for today: Dig into your own esource allocation between optimization and innovation. Are you spending more on incremental improvements to existing offerings or breakthrough development for emerging needs?

In markets under pressure, the temptation is always to cut “risky” innovation spending first. Instead, have a good think on whether the real risk lies in maintaining status quo approaches while more agile competitors redefine your category around you.

Is your industry feeling pressure to choose between investor demands and innovation investment?

Are you using AI aggressively to speed innovation?

Tap that reply arrow and share how you’re navigating the tension between financial optimization and product advancement.

Or reach out to my team of innovative product strategy consultants at Graphos Product.